The Coming Wave of Loan Maturities and Distressed Debt Opportunities

The next few years will test the resilience and creativity of real estate investors. As the post-pandemic lending cycle matures, a tidal wave of commercial real estate loans – many written during the low-rate era of 2019 to 2021 – is approaching maturity. Interest rates have more than doubled since those loans were originated, and values in several property types have corrected sharply. The result: billions in loans that can’t be refinanced conventionally, setting the stage for one of the largest distressed-debt opportunities in more than a decade.

A Perfect Storm in the Capital Stack

According to major data providers, roughly $2 trillion in commercial real estate debt will mature between 2025 and 2027. The problem isn’t just the volume – it’s the mismatch between today’s debt costs and yesterday’s valuations.

Take a multifamily property financed at 65% loan-to-value in 2020 at a 3.5% interest rate. That same loan refinancing today at 7% interest would see debt service increase by roughly 50–60%. Even if rents grew modestly, the property’s debt yield and DSCR have likely fallen below lender thresholds. Office and retail assets face an even sharper challenge, with values down 20–40% in some markets.

Traditional banks, under regulatory pressure to reduce commercial exposure, are tightening underwriting standards and limiting leverage. This leaves many owners stuck – unable to refinance, but unwilling or unable to sell. Enter private credit funds, opportunistic investors, and family offices looking to fill the gap.

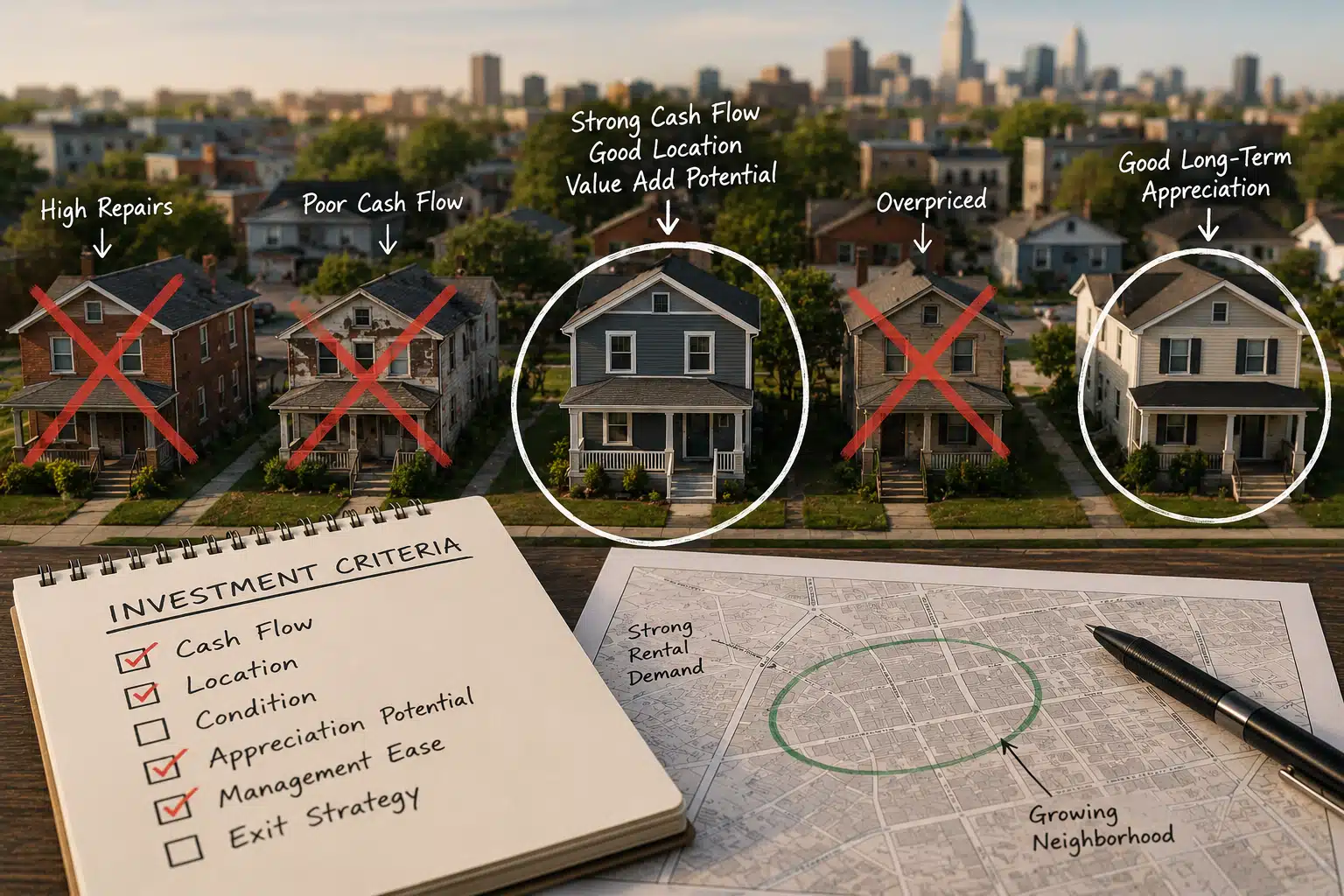

Distress Doesn’t Mean Disaster

It’s easy to assume “distressed” means “broken,” but that’s rarely the case in early-cycle dislocations. Many of these assets are fundamentally sound – they’re simply misaligned with the current capital environment. For seasoned investors, this creates several distinct opportunity profiles:

-

Performing but Unrefinanceable Loans: Owners with good occupancy and cash flow but insufficient DSCR for conventional refinance. These can be recapitalized through preferred equity, mezzanine financing, or private debt placements.

-

Discounted Note Purchases: Buying loans directly from lenders at a discount—often 70–90 cents on the dollar—then working out repayment with the borrower or taking title through a cooperative deed-in-lieu.

-

Recapitalization and Rescue Capital: Providing equity or structured capital to sponsors facing maturity defaults. These “rescue” structures often earn double-digit current yields plus equity kickers.

-

Direct Acquisitions Post-Workout: Once loans are resolved, many lenders will liquidate foreclosed assets. Investors prepared to step in early with capital and operational capability can buy below replacement cost.

Each strategy carries its own blend of return, complexity, and risk. The key is understanding where you want to play in the capital stack – and where your expertise adds real value.

How the Smart Money Is Positioning

Institutional investors are already mobilizing. Private credit funds have raised record levels of dry powder, often targeting transitional bridge debt or non-performing loan (NPL) portfolios. Hedge funds and family offices are forming partnerships with operators who can step into assets quickly, manage workouts, and reposition properties.

Smaller investors are not shut out. Many regional banks and CMBS servicers are quietly selling individual notes or small pools. Local operators with cash reserves or strong private capital relationships can compete effectively in this space, particularly in secondary and tertiary markets where institutional players have limited reach.

The difference between those who profit and those who perish in this cycle will come down to speed, creativity, and underwriting discipline. Investors need to understand not just the property’s value, but the lender’s position—what their regulatory pressures are, how their reserve requirements affect their decision-making, and what timing constraints they face.

Risk and Reward in an Uncertain Market

Distressed investing is not for the faint of heart. Loan workouts can be lengthy and unpredictable. Borrowers may litigate, tenants may flee, and municipalities may delay approvals. But with those risks come asymmetric return profiles.

A discounted note at 80 cents on the dollar that ultimately pays off at par can generate equity-like returns with collateral-backed downside protection. A well-structured rescue capital deal can yield 12–18% annualized returns with a short-duration exposure. Direct acquisitions from distressed sellers can lock in long-term basis advantages that pay dividends for years.

The discipline lies in underwriting conservatively. Assume longer hold periods, higher cap rates, and additional carry costs. Stress-test both exit values and refinance rates. And, perhaps most importantly, align with legal and financial advisors who have lived through prior downturns—workout expertise is an art as much as a science.

The Bottom Line

Every market cycle produces its own breed of opportunity. In 2008, it was bank-owned REO sales. In 2012, it was value-add multifamily. In 2020, it was industrial and logistics. The next wave will be distressed debt and recapitalization – assets with strong fundamentals but broken capital structures.

For small and mid-sized owners, this may mean acquiring one-off deals from local lenders. For institutional investors and hedge funds, it may mean deploying into structured credit or forming joint ventures with distressed operators. The scale differs, but the principle is the same: liquidity plus conviction creates value.

The coming wave of maturities will test every assumption investors have made about leverage, liquidity, and timing. But for those with dry powder and discipline, it’s not a threat – it’s the next great opportunity.