Surviving the Lending Squeeze When Raising Capital for Investment Real Estate

Lending and mortgages—more changes lie ahead

We can all agree that the troubles with the mortgage industry began in 2020 with the unexpected coronavirus pandemic. Throughout the last two years, we’ve navigated a turbulent economy, yet what we face now and into the near future is an unprecedented squeeze in lending practices and availability of capital for investing.

In this article we’ll talk about why these factors have gathered to create a perfect storm of challenges for real estate investors. We’ll also offer a few alternative lending sources so you can leverage capital to secure your next property.

The pandemic, inflation and a slow-to-respond Fed

When we entered the pandemic in early 2020, thanks to the Fed’s response to the crisis, interest rates dropped. Brooking’s talks about the factors that occurred during the onset of the pandemic as it began to impact the economy, saying, “The Fed cut its target for the federal funds rate, the rate banks pay to borrow from each other overnight, by a total of 1.5 percentage points at its meetings on March 3 and March 15, 2020. These cuts lowered the funds rate to a range of 0% to 0.25%.”

Brooking’s goes on to share more decisions made by the Fed to combat the unprecedented impact of the virus. Rate drops made mortgage lenders very busy, with many homeowners refinancing and investors’ creative strategies as they leveraged capital through HELOCs, refinancing and other practices. Property owners who took advantage of this window of low interest rates secured mortgages at record-low levels. The housing market grew in opportunities, but so did home prices due to supply and demand. Money was readily accessible at a low cost, and more people became property owners than ever before.

And then came inflation. Factors influencing inflation included government-driven fiscal support packages, workers changing their jobs or leaving their jobs causing a shift in the workplace economy, extended supply chain disruption, a loose monetary policy and governmental over-spending. (There are many other factors, some political, some global, yet the changes are felt by every American on a daily basis.)

How did the Fed deal with inflation?

Prior to the biggest (.75 bps) Fed rate hike on June 15, 2022 there were two smaller rate hikes in 2022. Many believed the Fed acted too late in response to the rapid inflation rate since they argued that inflation was “transitory” throughout 2021. Now that mid-year 2022 inflation has triggered what many are saying is a pending recession, the Fed is reacting with larger than normal rate hikes. This is causing a lot of volatility in the market, and lenders are tightening their belts.

Trading Economics quotes the Fed chair as saying, “Powell also said the central bank will be looking for moderately restrictive level by the end of the year, meaning a 3% to 3.5% level for the fed funds rate.”

Fed Funds Rate over the last 10 years:

Mortgage lenders tighten policy

The mortgage industry is reacting to the Fed’s aggressive rate hikes and with the continuing housing shortage, the landscape of real estate investing is changing rapidly. Several of the shifts occurring with lenders include:

-

Closer scrutiny of lending practices and evaluation of credit reports

-

Stricter income requirements for applicants

-

More aggressive income-verifying practices

-

Longer pre-approval and originating timeframes

-

More resistance to self-employed or employment gaps

-

Lenders are looking at applicants holistically regarding risk

-

Lenders are assessing properties as well as applicants more closely before approving

-

Lenders are adding “fine print” safety nets such as prepayment penalties and eliminating rate buy-downs

-

Many banks are still not resuming originating HELOCs

-

Shifting focus to cash-out refinances and other products

Higher housing costs means that applicants need to request higher mortgage amounts, making it more difficult to get approved. Lenders are stating these increased restrictions are due to low consumer confidence, concerns about the housing market stability and unemployment among others, citing lessons learned from prior financial crises.

What does this mean for real estate investors?

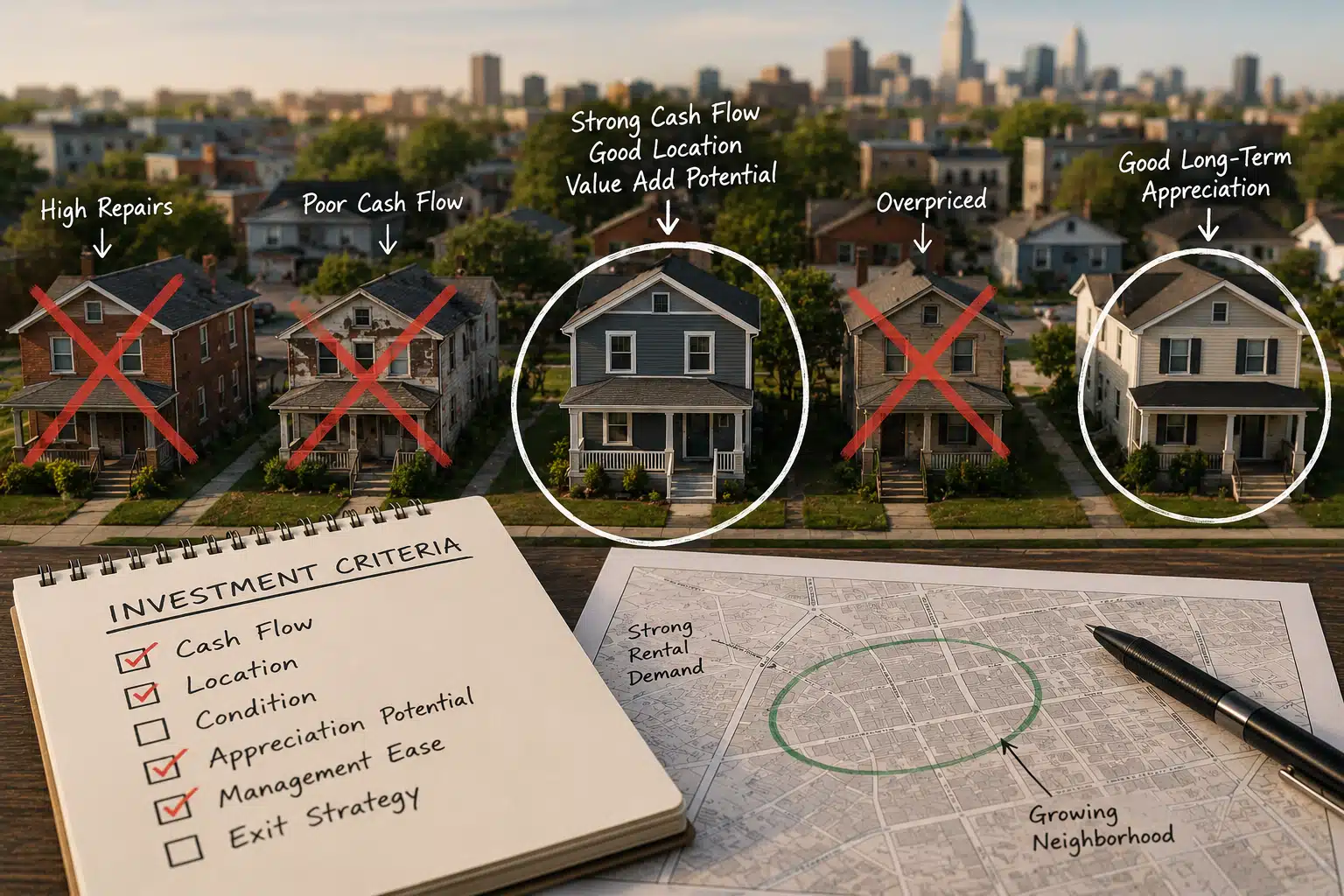

With the mortgage banking industry on its heels and in a deeper “preserve and protect” mode, there are still ample opportunities for raising capital and using “other peoples’ money” (OPM) to secure your first or next investment property. As homeowners become distressed, properties become available. As other investors shift their portfolios for new opportunities, properties become available. As the housing market normalizes in supply and falling prices, properties become available. The key is finding creative ways to raise or leverage capital so you can take advantage of these opportunities when they happen.

Obviously, cash is king. But are there ways to be more creative in sourcing your financing? Leveraging existing property value to generate more creative ways to finance your next deal? How can you use “other peoples’ money” (OPM)? Here are a few alternatives to help you be creative in finding the best way to finance your next property:

-

Seller financing is a method in which the seller holds a note for you. You can do it via an equitable title which allows the buyer to use and possess the property in lieu of ownership of the property as no deed is transferred. The other method is traditional seller financing, where the ownership is transferred and the seller acts as the bank in a free-and-clear situation. From a seller’s perspective, equitable title helps the seller possibly reduce tax risk. Plus, if the buyer doesn’t make good on the payments, you can kick them out. In default where the deed was transferred the seller can foreclose on the property. Foreclosing, however, is costly to a seller.

-

Lease purchase agreements is another type of seller financing. The seller gives the buyer equitable title to the property and gets credit for partial or full lease payments. There’s also a “leaseback” option where you can pay toward ownership via rent, however it can be a longer process to become the property owner.

-

Hard money lending is where the lender is using the property as collateral. They’re more interested in the property than the party. Traditional lenders look at the person and their ability to repay the mortgage and avoid default. The benefits of hard money loans is more for experienced fix-and-flippers as they can also incorporate the rehab costs into the purchase costs. When you build a relationship with a hard money lender, you can avoid down payments if you build trust. The closing timeline is a lot shorter with hard money lenders. Traditional loans can take up to 45-60 days, where the hard money lender may have the cash on hand in a little as 30 days. There’s also not as much documentation in hard money loans. On the flip side, hard money loans often come with a much higher interest rate because the lender wants to make a profit. It’s a short-term loan, and you have to stay inside that time frame. Hard money loans are best for fix-and-flips to sell or refinance.

-

Government-backed loans The Federal Housing Authority (FHA), U.S. Department of Agriculture (USDA) and Veteran’s Administration (VA) loans make up the bulk of government-backed loans which originate with private lenders but are insured by the US Government. The loan process is longer because they do a lot of due diligence such as surveys, rent analysis studies, environmental studies, etc. The time frames vary, but 60-90 days is typical to get to closing.

-

1031 Exchanges are an untapped strategy for many long-term investors. 1031 Exchanges provide tax breaks allowing real estate investors to scale since you can buy an investment property, sell it and then buy another one and defer the capital gains. You just continue to acquire real estate. More details are in our EIC article: “1031 Exchanges—Tips For Success”

SDIRAs, HELOCs, insurance policies, commercial banks are a few other alternative sources for financing. The key item to remember during economic downturns where interest rates and inflation command the headlines is that banks want safe mortgages. They want to reduce risk in a volatile economic environment and will scrutinize loans more than ever. Build relationships with your lenders, whether they’re traditional banks, mortgage brokers or hard money lenders. Your professional practices as a real estate investor and cultivated relationships with lenders will earn the trust you need to secure the financing for that next property.