Fed Cuts Rates, But Mortgage Costs Climb: What Real Estate Investors Need to Know

The Federal Reserve’s recent interest-rate cut might sound like good news for borrowers, yet mortgage rates have defied expectations and climbed higher. For real estate investors, this divergence between policy rates and borrowing costs raises critical questions: how will it affect deal flow, financing strategies, and portfolio performance? Understanding the forces behind the gap—and the steps you can take to manage the risks—is essential to protecting returns in the months ahead.

What We Know

From recent reporting:

-

The Federal Reserve lowered its benchmark (federal funds) rate by 0.25 percentage points — its first cut in quite some time.

-

Despite that cut, mortgage rates (especially on longer-term fixed loans) have not declined, and in many cases remain elevated. Some rates even ticked up.

-

One big reason: mortgage rates are influenced more by long-term expectations — inflation, long-term Treasury yields, perceptions of future Fed moves — than by short-term interest rates.

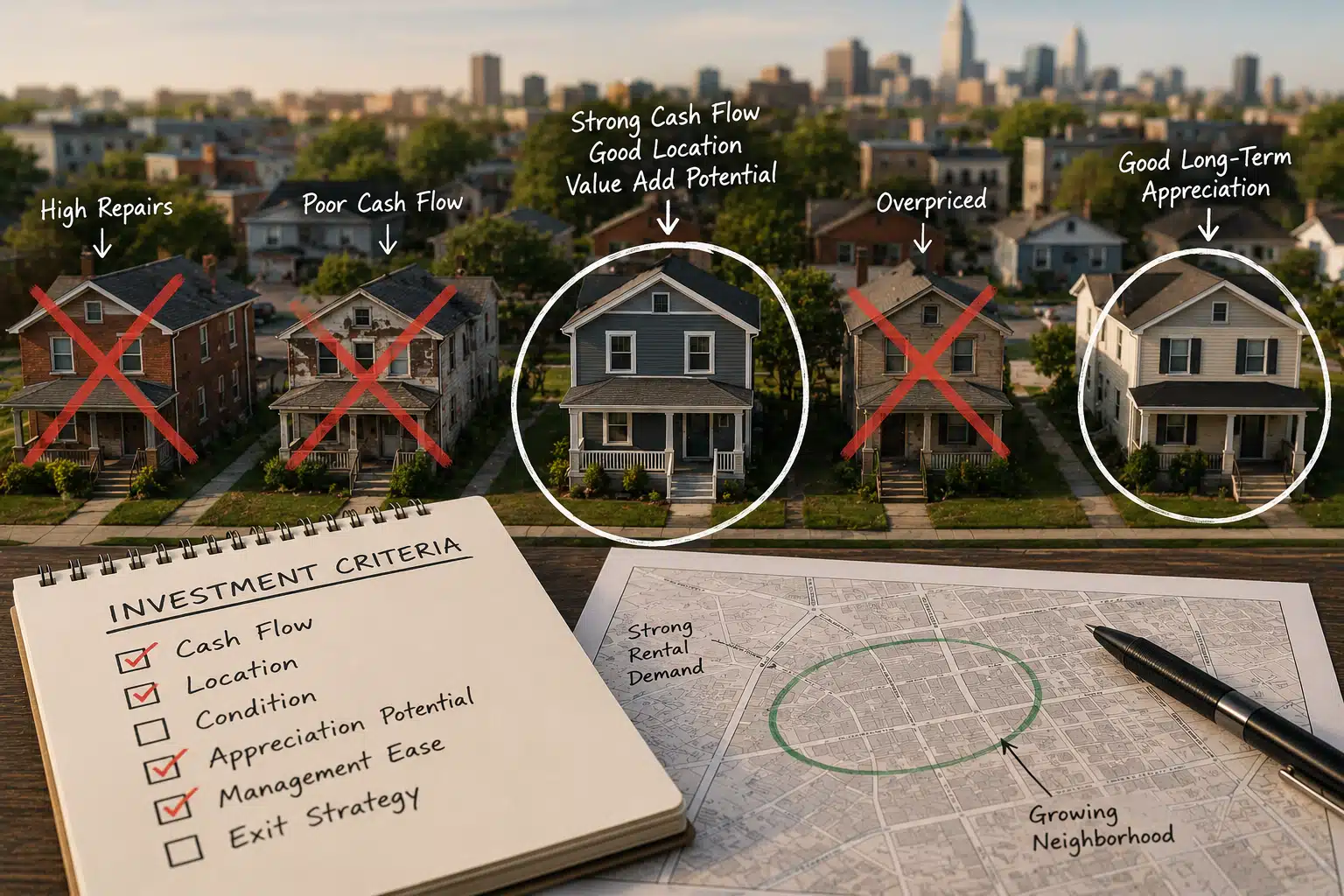

What This Means for Real-Estate Investors

Here are ways the divergence between the Fed rate cut and mortgage rates being high (or rising) can affect you, both positively and negatively.

Negative Impacts

-

Financing Costs Still High for New Deals

-

Even though the Fed’s cut is intended to ease monetary policy, if mortgage rates (especially longer-term fixed mortgages) remain elevated, borrowing for purchases or refinances can remain costly. That can squeeze margins on deals or reduce yield when locking in long-term debt.

-

-

Uncertainty in Cost Projections

-

Because mortgage rates are being driven by macro-factors (inflation expectations, bond markets), they may be more volatile. If you’re projecting acquisition costs, rehab costs, or carrying costs, those financing cost assumptions might need to be more conservative.

-

-

Lock-in Effect for Sellers and Buyers

-

Current homeowners with low fixed rates are less likely to sell and take on a higher rate, reducing inventory. That can limit opportunities for investors who rely on purchasing existing homes. At the same time, buyers may be priced out unless rates come down more meaningfully.

-

-

Refinancing Isn’t Always a Win

-

Some deals to refinance may not make sense unless the rate differential is significant enough to offset closing costs and fees. If mortgage rates don’t drop enough, many owners will stay put with existing debt rather than refinance. This can limit cash-flow improvements via financing maneuvers.

-

Positive / Moderating Impacts

-

Fed Cuts Could Eventually Put Downward Pressure on Mortgage Rates

-

Though mortgage rates’ movement doesn’t immediately follow Fed actions, rate cuts can help, especially if they shift expectations for future inflation and growth. If markets believe further easing is coming, long-term yields might drift down. Over time, that could lead to better financing opportunities.

-

-

Selective Use of Adjustable-Rate or Short-Term Debt

-

For investors with flexibility, using adjustable-rate mortgages (ARMs) or shorter-term fixed rates may allow locking in somewhat lower costs until fixed rates fall. But these come with risk, especially if inflation or rates rise.

-

-

Potential Bargains Where Buyers Hesitate

-

Inventory may be tight or sellers may be locked into current mortgages, but in some markets investors may find less competition, or bargains where properties are undervalued due to rate-shock effects. For those with cash or strong financing, opportunities may emerge.

-

Key Risks to Monitor

-

Inflation Trends: If inflation remains stubborn, long-term interest rates may stay high or even rise, lifting mortgage rates despite Fed cuts.

-

Bond Market Behavior: Treasury yields are very important. If yields rise (due to inflation or supply concerns), mortgage rates generally follow.

-

Economic Data: Employment, wage growth, consumer spending — if strong, could keep rates up. But weakening could help lower them.

-

Fed Guidance and Market Expectations: If the Fed signals fewer cuts than expected, markets may adjust, pushing yields up. Confidence in future policy matters.

What Investors Should Do / Strategic Moves

Based on all this, here are some actionable ideas:

-

Lock in Financing When You Can

-

If you have an attractive fixed rate available, consider locking it before further upward pressure on rates emerges.

-

-

Use Hedging / Interest Rate Caps Where Appropriate

-

For variable rate debt, explore interest rate caps or structures that limit your exposure if rates rise.

-

-

Stress Test Cash-Flow Models

-

Incorporate higher interest rates and higher debt service in your spreadsheets. What happens to your margins if mortgage rates stay elevated for another year?

-

-

Consider Shorter Horizon Deals

-

If you believe rates will fall in the medium term, short-term holds or flipping may make sense over long-term buy-and-hold, especially where financing is expensive.

-

-

Keep An Eye on Markets Where Rates Have Dropped More

-

Mortgage rates vary by region, lender, borrower credit quality. Get quotes from multiple sources; sometimes certain markets or lenders offer relatively better terms.

-

-

Watch Treasury Yields & Inflation Reports

-

Because mortgage rates are sensitive to these, staying on top of 10-year Treasury yields, inflation data (CPI, PCE), Fed minutes, and forward guidance give clues when mortgage rates may ease.

-

Bottom Line

For now, Fed rate cuts are a necessary but not sufficient condition for lower mortgage rates. As a real-estate investor, you should anticipate that financing costs may stay elevated for a while, even with Fed easing. That changes how you evaluate deals:

-

Be more conservative with your financing assumptions.

-

Push hard to lock in favorable financing where you can.

-

Carry more margin for error in your projections.

-

Be opportunistic in markets/lenders that are shaving off costs.